I Built an AI System That Makes Timestamped Market Predictions

Every analyst has an opinion on the market. Almost none of them timestamp it, track it, and publish whether they were right.

This is the core problem with market analysis today. Not a lack of information. A lack of accountability. Analysts issue vague calls (“we see headwinds for tech”), shift the goalposts when they’re wrong, and quietly delete the tweets that didn’t age well. There’s no public record, no scoring, no consequences.

I wanted to test a question: if you point AI at the full firehose of financial news and force it to take structured, falsifiable positions, can it actually beat the noise? So I built a system to find out. Signal Rundown is an AI that reads 22+ financial sources every 2 hours, maintains explicit bullish/bearish/neutral positions on every stock it tracks, and makes timestamped predictions with specific price targets and deadlines. Every prediction gets scored against actual market data. No editing. No deleting. The record is permanent.

What It Actually Does

Signal Rundown is not a chatbot and not a news aggregator. It’s a signal extraction system that runs continuously.

Every 2 hours, the system pulls from 22+ sources (RSS feeds, Google News, financial data APIs) and filters aggressively, because most financial news is noise. The articles that survive get their full text extracted and run through LLMs that decompose each one into structured signals: direction, key facts, sentiment, which companies are affected. This matters because raw articles are ambiguous. A single earnings report might be bullish for the company, bearish for a competitor, and neutral for the sector. The extraction step forces a position.

Those signals accumulate into entity states: a rolling analytical position per stock that updates as new evidence arrives. When a position reaches sufficient conviction, the system generates predictions with a specific direction, baseline price, expected move range, and target date. These span 1 week, 1 month, 1 quarter, and event-driven horizons.

The tech stack is Python, PostgreSQL, and LLMs. The whole system runs on a single Railway instance. Collection happens every 2 hours from 5 AM, entity states update on the same cadence, and a daily brief goes out at 6 AM Pacific.

What Makes It Different

Most analysis is stateless. Someone publishes a take, it floats around for a day, and it’s forgotten. No one checks whether it was right. Signal Rundown works more like a real analyst: it maintains views, updates them as evidence changes, and its track record is permanent. Every entity has a living analytical state that accumulates evidence over time. When the system flips from bullish to bearish, that shift is logged with the specific signals that caused it.

The difference is scale and discipline. Signal Rundown does this across 700+ entities simultaneously, processes information in minutes instead of days, and never has a bad Monday.

The key architectural decision: predictions are first-class objects, not chat responses. Each prediction records a baseline price at the time of the call, an expected move range, and a target date. When that date arrives, the system automatically scores the prediction against the actual price. Correct or incorrect, the result is public.

Early Results

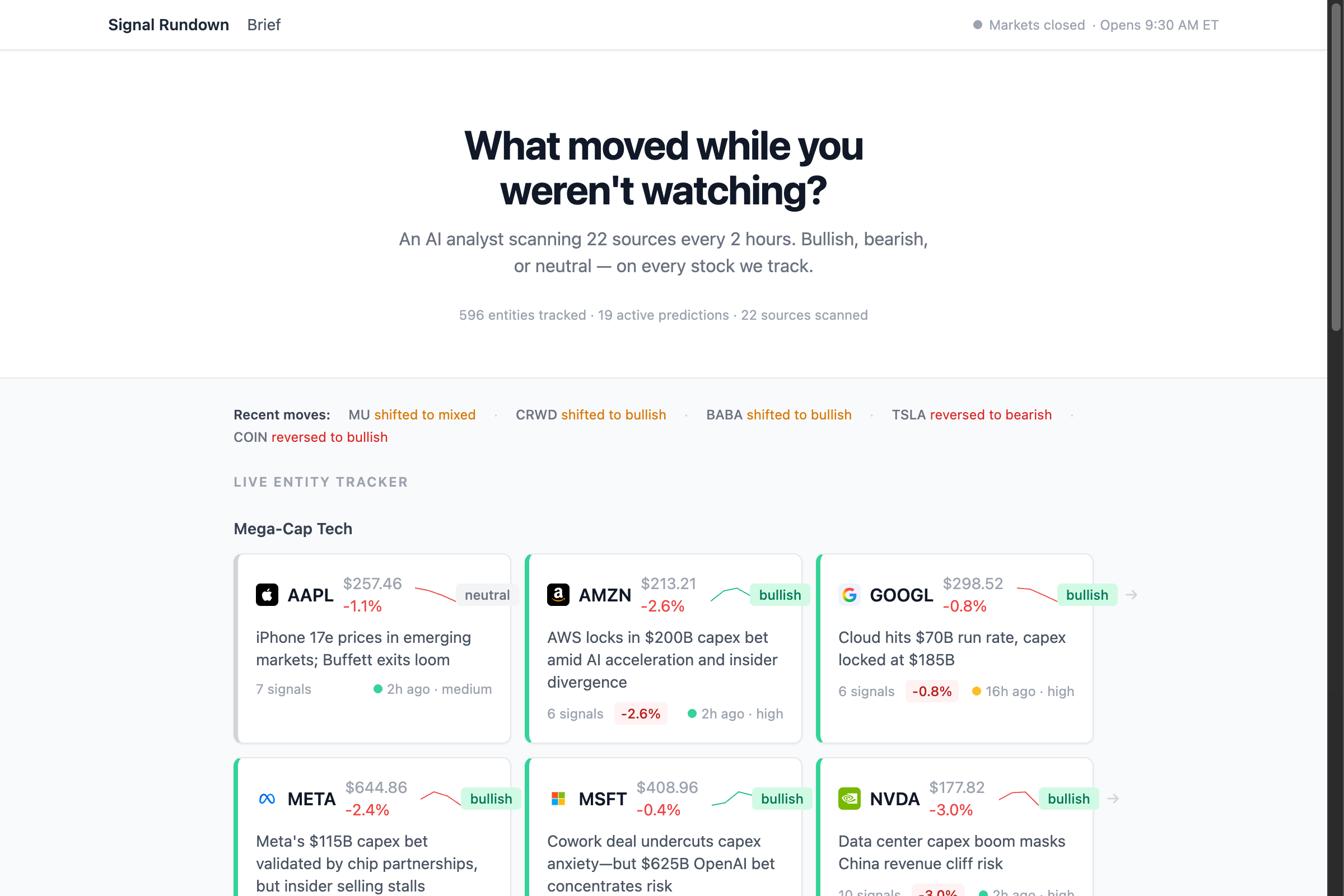

The system has been running in production for several weeks. Here’s what the landing page looks like:

Each card shows a stock’s current position (bullish/bearish/neutral), the latest price, a one-line thesis, and how fresh the analysis is. The “Recent moves” ticker at the top shows position changes as they happen.

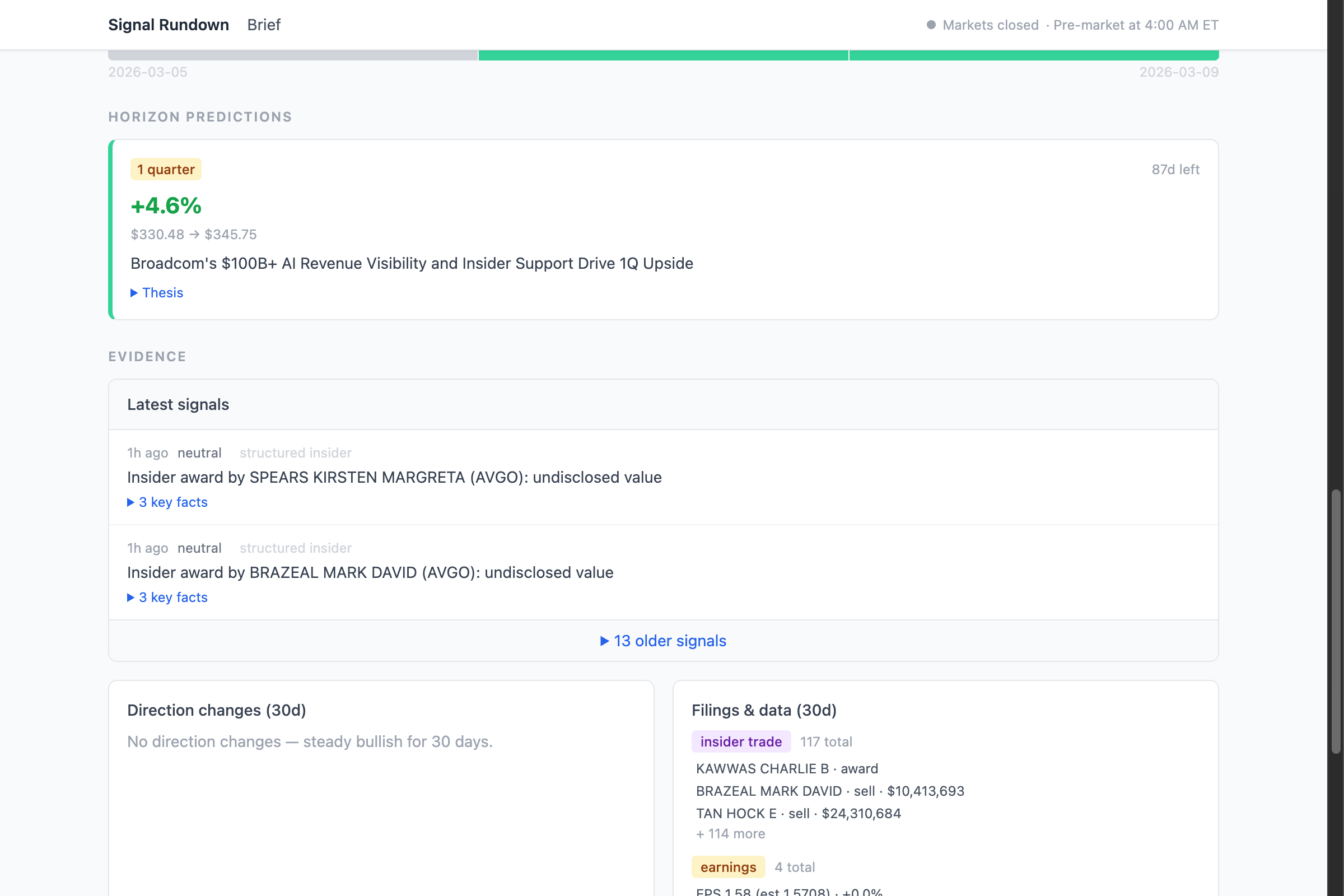

Drilling into any entity shows the full analysis. Here’s Broadcom (AVGO), where the system is currently bullish with high conviction:

The entity page includes the full analytical state, fundamentals (market cap, P/E, insider activity, analyst consensus), and active predictions with live P&L tracking.

Here’s what a live prediction looks like. This is AVGO’s 1-quarter prediction, recorded at $330.48 on March 5:

Baseline price, current price, live P&L, days remaining, and the thesis that generated it. When the target date hits, the system scores it automatically.

Some numbers from production:

- 22 sources scanned every 2 hours

- 700+ entities with live analytical positions

- 16,000+ articles processed in the last 30 days

- 14,000+ structured signals extracted

- 18 active predictions with specific price targets and deadlines

Predictions started recording on March 6. The track record is young. I’m not claiming accuracy yet. The point isn’t “we’re already right.” The point is I’m building a system that will prove whether it works, because every call is recorded and scored. Most systems never submit to that test.

What’s Next

Three things I’m focused on:

Scoring the first batch of predictions. The earliest 1-week predictions will start hitting their target dates mid-March. This is the first real test of whether the system’s signals translate into predictive accuracy.

Building in public. The entity tracker is live at signalrundown.com. I’ll be posting prediction scorecards and interesting position shifts on @signalrundown on Twitter.

Expanding the evidence base. The system currently reads news and financial data. Next up: 13F institutional holdings filings, short interest data, and earnings transcript analysis. More structured data makes better predictions.

If you want to follow along, check out signalrundown.com or follow @signalrundown.